The Biggest Money Mistake I Was Making Before Reading Rich Dad Poor Dad

I used to think money was simple: you work hard, you earn more, you buy stuff, and you’re suddenly rich. Sounds silly when I write it down, but I believed it for years. My days were a loop of paycheck, loan, and another purchase I barely needed. Then I cracked open Rich Dad Poor Dad, and everything started shifting. Not with a dramatic lightning bolt, but with small, honest questions I’d ignored for far too long.

If you’re curious about changing your money story, I’ll share what I learned and how it changed my life—and my budget. And yes, I’ll drop a link to the book that started it all: Rich Dad Poor Dad.

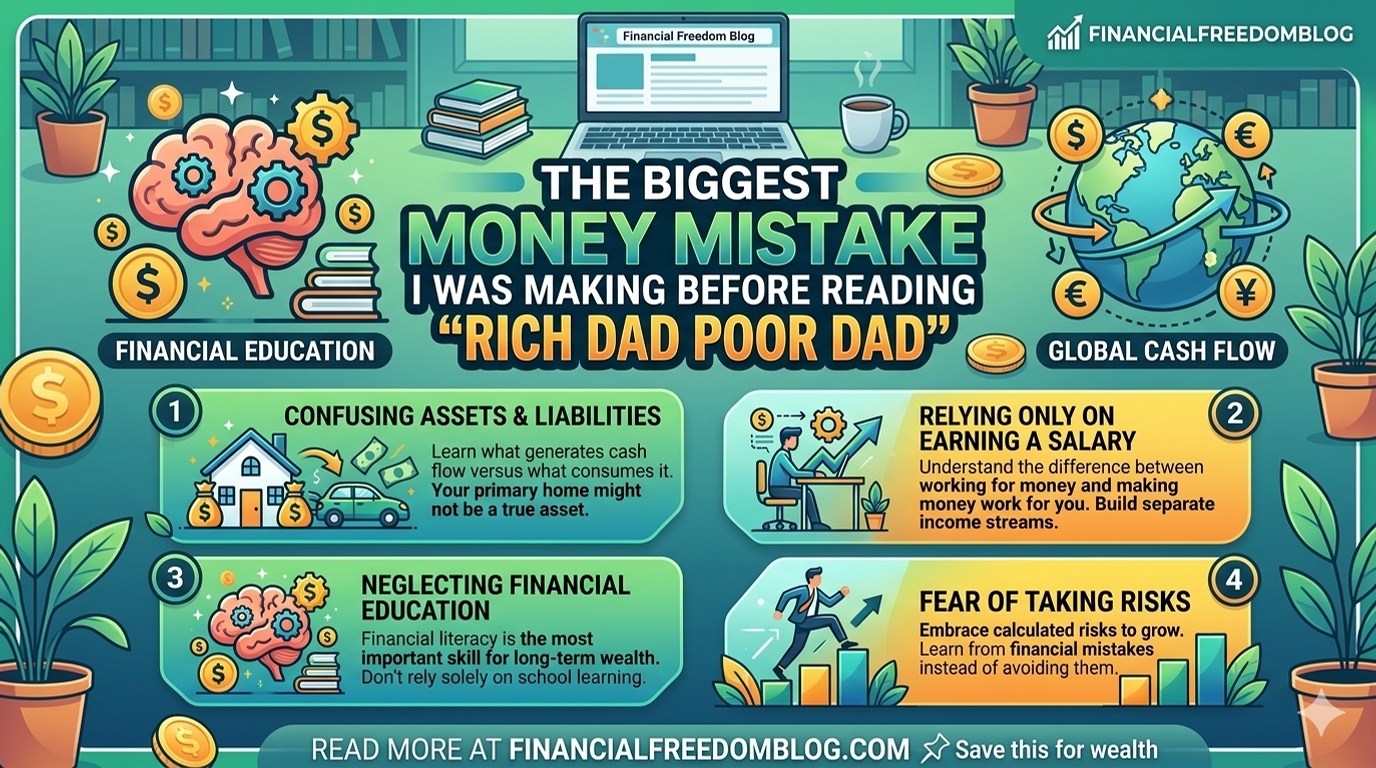

What I was doing wrong (the heavy, costly habits)

- Chasing status with credit cards. I’d buy the newest gadget or outfit to feel like I belonged, then pay the price of interest for months.

- Treating my salary like a reward rather than a tool. I spent first, saved what was left, which was basically nothing.

- Believing debt was a short-term convenience. I didn’t realize it was a long-term tether slowing my wealth-building.

- Ignoring assets and investing. I bought liabilities—things that lost value or required ongoing money—rather than things that could grow my money.

- Relying on luck instead of learning. I avoided building financial literacy because it felt intimidating, or maybe a little boring.

What Rich Dad Poor Dad taught me in plain language

- Assets put cash in your pocket. Liabilities take it out. Simple, but life-changing when you measure every purchase by that rule.

- Cash flow is king. I finally stopped chasing big paydays and started building streams of income that don’t require me to trade time for money.

- Financial education beats a bigger paycheck. It isn’t about how much you earn; it’s about how well you manage what you already have.

- Think like an investor, not a spender. Small, steady bets on assets beat big, impulsive buys that drag you down later.

A little Canadian twist I’m not afraid to admit

Back home in Canada, I love a good Tim Hortons run. It’s comforting, familiar, and expensive enough to matter. One winter, I walked out of the cafe with a latte, a receipt, and a new sense of anxiety about debt. I realized I wasn’t budgeting for future me—I was just budgeting for today’s crave. The habit wasn’t heroic; it was a money drain. Reading Rich Dad Poor Dad gave me a wake-up call that carried into my daily life—how I spend on coffee, groceries, and groceries I pretend I don’t buy all add up.

My simple, pragmatic steps I started using right away

- Track every dollar for 30 days. No excuses, no edits. Just truth.

- Automate savings before I touch anything else. Even a little builds momentum.

- Shift from consumer debt to investment in assets. I prioritized things that could grow my money, not drain it.

- Prioritize financial education. I read, I listen to experts, I ask questions, and I test ideas in small ways.

- Create a basic budget with an asset-first mindset. It’s not about restriction; it’s about freedom to choose.

The ripple effect: why this matters for beginners

When you start treating money as a tool—not a source of identity—you stop living paycheck-to-paycheck. You begin to see how small, smart choices compound. The biggest mistake I made was pretending I didn’t have control. The truth is: you can control a lot more than you think, with a plan that fits you and your life, even if you’re in Canada and love hockey on Friday nights.

A relatable book to pair with the journey

If Rich Dad Poor Dad sparked something for you, try Your Money or Your Life by Joe Dominguez and Vicki Robin. It pairs beautifully with the Rich Dad mindset—clarity about what money means to you and how to align your spending with your values. It’s practical, reflective, and perfect for anyone starting out on a path to financial independence.

Ready for the next step? I’ve got you covered

If you’re ready to dive deeper, this is a quick start I’d actually recommend:

- Read Rich Dad Poor Dad to reshape how you think about money and assets. Download Rich Dad Poor Dad and start the journey today.

One more tiny nudge: keep it simple and stay curious

Money growth doesn’t have to be dramatic. It can be steady, teachable, and surprisingly satisfying. I kept the habit simple: learn a little, apply a little, repeat. Before long, I stopped saying “I can’t afford it” and started saying “I’ll invest in it smarter.” If you’re ready to try, click that link above and give your financial education a real chance.