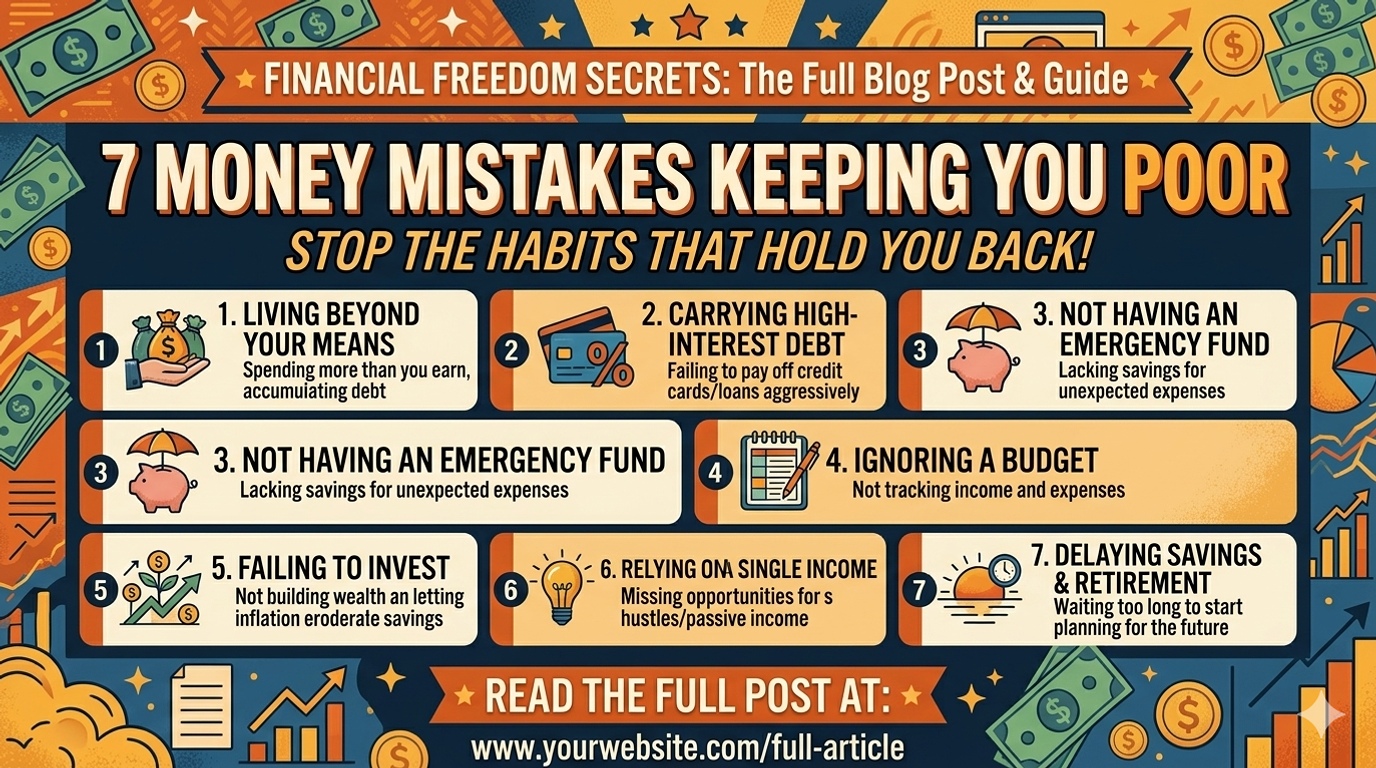

7 Money Mistakes Keeping You Poor

I'm not here to judge you. I’m here because I’ve made these same blunders, sometimes more than once. In Canada, where prices drift upward and winters feel endless, small money habits can swing your wallet big time. The good news? Tiny, doable changes plus a little know-how can flip the script. You’ll see what I mean as we dive in, story by story, tip by tip.

Here’s a little personal context to keep it real: I grew up in a small town outside Vancouver. We biked to the rink, snagged a Tim Hortons coffee on weekends, and pretended the loose coins in our pockets weren’t really a problem. Then reality hit—rent, groceries, and a car repair bill all in the same month. I started paying attention to where every dollar went. That awareness didn’t just save me; it gave me choices. And if you stay with me here, I’ll help you find those same choices in your own life, eh?

1. Not having a real budget (you know, the boring one that actually works)

- Track every dollar for at least 30 days. Yes, even the loonie you drop in the vending machine.

- Use a simple framework (like 50/30/20) or a budgeting app so your plan lives in your phone, not just in your head.

- Schedule a weekly 10-minute money check-in. Short bursts beat long, guilt-ridden sessions later.

2. Living beyond means with credit cards

- Don’t carry a balance on high-interest cards. If you must, pay more than the minimum each month.

- Automate a monthly payment to yourself—treat savings like a bill you must pay.

- Use the “one-in, one-out” rule for big purchases: if you buy something new, you fund it by selling or letting go of something unnecessary.

3. Ignoring debt and high-interest traps

- List debts from highest to lowest interest. Attack the top one first with a targeted plan.

- Resist new debt for non-essentials. If it isn’t building your future, it’s probably not worth it.

- Consider a snowball or avalanche method—pick the approach that keeps you motivated.

4. No emergency fund (the mom-and-pop safety net)

- Start with a tiny goal—$500 or $1,000. Then grow to 3–6 months of living expenses.

- Automate monthly transfers to a high-interest savings account. Out of sight, out of mind, in your bank’s favor.

- Keep it liquid. You’ll use it, not borrow against it.

5. Wasting money chasing shiny objects instead of investing

- Pause before buying into every gadget or trend. Ask: “Will this help me earn money or save more?”

- Put a portion of every paycheck into investing, even small amounts add up over time.

- Learn the basics of low-cost index funds or diversified portfolios rather than flashy schemes.

6. Skipping retirement planning or not starting early enough

- Open a TFSA and/or RRSP and contribute automatically. The power of compounding is a long game in your favor.

- Increase contributions by a small percentage each year—don’t wait for a perfect moment.

- Review fees, tax implications, and beneficiary details so your money isn’t quietly eating itself away.

7. Underinvesting in financial education

- Read, listen, and ask questions. Financial literacy is a skill you can improve, not a trait you’re born with.

- Take a course, listen to money podcasts, or chat with a friend who’s good with money. Small, regular learning beats big, rare dives.

- Build a simple money playbook: your budget, your debt plan, your savings target, your investing starter kit.

Ready for a mindset shift that actually sticks? I’ve found a book that helped me reframe money as a tool, not a stressor. If you’re open to changing how you think about wealth, download Rich Dad Poor Dad and start moving from paycheck to purposeful progress. It’s not a magic spell, but it’s a sturdy ladder you can climb with daily habits and smarter choices.

And if you’re curious about what’s trending in personal finance today, you’ll notice more focus on budgeting clarity, automatic savings, low-cost investing, and financial literacy for beginners. These aren’t buzzwords; they’re practical steps you can take this week. So pick one tiny habit, stick with it, and watch how your financial story begins to change—one updated budget, one debt payment, and one smarter investment decision at a time.